Paul Goldsmith: Why is it important that the Government gets back to surplus and starts repaying debt?

Hon BILL ENGLISH: Although the level of Government debt is well below that of many other Governments that we compare ourselves with, it is important that we keep Government debt low in order to offset very high household debt and to ensure that we can manage through another recession. Net Government debt is still rising today by around $130 million a week and will reach $70 billion in 2016-17, up from around $10 billion just 5 years ago. That is the equivalent of around $15,000 for each and every New Zealander. We simply believe that it would be prudent to return Government debt to lower levels so that we are better able to reduce the pressure on interest rates rising sooner than they otherwise would, and reduce pressure on an exchange rate that is already higher than is comfortable for us.

Economists will always remind you that there are trade-offs to be considered when making choices - in order to get more of something, we have to accept having less of something else. Now in this case, Mr. English "simply believes" it's better to make loads of spending cuts* that are actually depressing economic growth, affecting the lives of our most vulnerable citizens, and increasing unemployment (these are the trade-offs), in order to keep interest and exchange rates down for longer**.

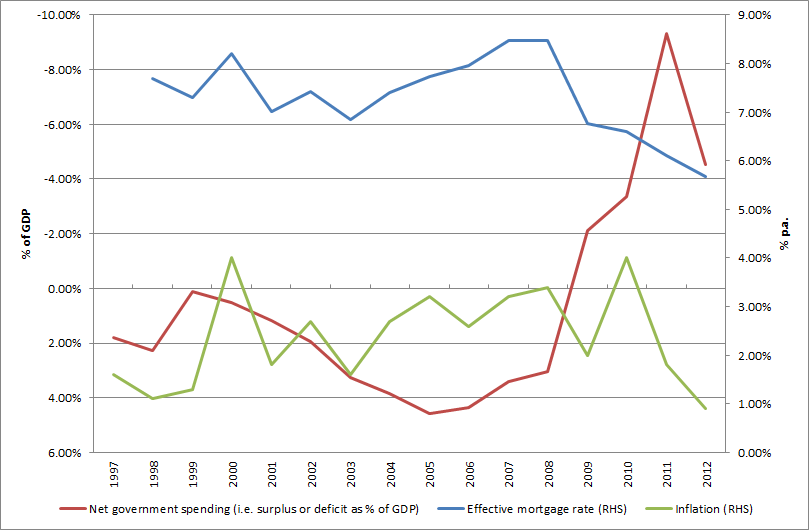

Is he really considering the trade-offs here? What are the real benefits of keeping interest rates down for longer? And even then, how much influence does government spending actually have on interest rates anyway? Looking at the chart below, there doesn't seem to be any such link between interest rates, inflation, and government spending over the last 15 years. In fact, interest rates came down at the same time as government spending spiked following the global financial crisis in 2008. You make up your own mind...

* For those of you that doubt the size of cuts that the National government has made over the past few years, my next post will show you how extensive they are.

** Incidentally, Mr. English has laughed off intervention in the exchange rate as proposed by opposition parties, but here he is implying that this is part of the reason for targeting surplus!