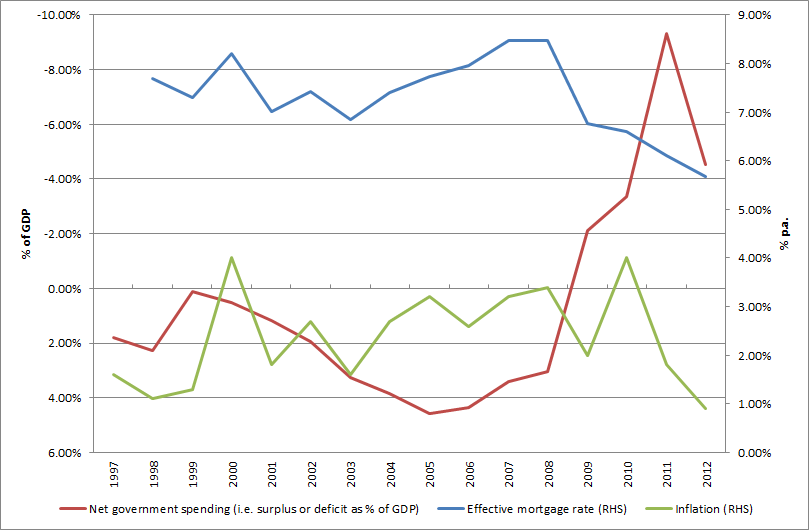

I have two questions relating to a recent editorial ("Future proofing", July 27).

1) What is the "fiscal crisis" that we need to avert? The treasury talks of a shortfall. But what does that mean? It simply means that the government's spending is projected to be more than its revenue in the future. Which means that the government will need to run deficits. So what? Our government (like the US, UK, Japan, Canada, and Australia) can actually run deficits in perpetuity. There is no hard constraint other than a self-imposed one. And I'm not talking about printing money here. All governments that have their own free floating currency can spend without constraint. The Treasury and RBNZ co-ordinate activities such that there is alwaysbuyers of government debt. From what I can tell, many economists don't know this and still think we live in a gold-backed currency world, which effectively ended in 1971. Today the government bond market really exists just to provide the private sector with risk-free savings!

The only real concern that the government has is the possibility of high inflation. If there is too much spending, without a comparable increase in production, then we will get inflation (or so the story goes). But we have to ask ourselves what is the likelihood of this given that a) we are in the biggest global downturn since the Great Depression; and b) there is idle capacity in our economy (just look at the unemployed). Japan has run big deficits for 20 years without any inflation and debt/GDP going to over 200%. And has the sky fallen in? No. Are they still providing excellent social services? Yes. In fact, Japan score very well on most of the measures that make up The Economist's Quality of Life index, and the UN's inequality measures.

2) Why don't we focus on the (lack of) reliability of long-term predictions? Even if someone can convince me that there is an impending fiscal crisis (unless we make sacrifices now), should we weigh so much on these forecasts from the Treasury? Inside an investment prospectus you will often see this disclaimer: "past performance does not guarantee future performance." We need to apply this to financial forecasts that come from economists too - and this includes staff at the Treasury! In general, they don't have a great track record. It's not their fault - it's just incredibly hard to predict the future!